If the Mayan apocalypse can be postponed (I am not sure exactly at which time it is supposed to occur so I may be speaking too soon here) then surely the U.S. Congress can agree to actions to avoid the fiscal cliff. Lawmakers are poised to give us over $500 billion in tax increases and over $100 billion in spending cuts to begin the new year. The fiscal cliff is a pretty big lump of coal as a gift to begin 2013.

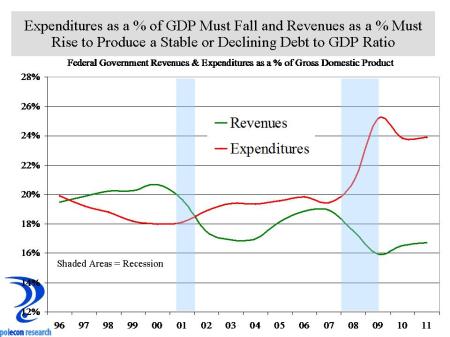

What is extraordinary about the cliff’s self-inflicted harm is that it appears almost all sentient beings realize what needs to happen. More importantly, there also appears to be substantial agreement on most of the actions necessary to avoid the economic harm resulting from the fiscal cliff. Spending clearly has to be cut just as surely as revenues have to be raised.

With so much apparent agreement on actions needed to avoid the damage, it is hard to understand the calculus of lawmakers as the lack of an agreement begins to demonstrably affect business and consumer confidence as well as financial markets. Congress always comes up with a temporary fix for the alternative minimum tax and can easily do so again. Almost everyone wants the payroll tax cut to expire (for different reasons – Republicans because they don’t like the temporary nature and believe it has no incentive for work and saving and Democrats because of its impact on the Social Security trust fund). There is little support for extending unemployment benefits. It seems like neither party really wants the spending cuts (Republicans opposed to defense cuts and Democrats to non-defense cuts). There is disagreement over the tax increase for high income individuals included in the Affordable Care Act and Medicare reimbursements for doctors but those are a miniscule portion of the cliff’s effects. Beyond all the posturing, the fight in congress is really about whether to extend tax cut provisions to 98% or 100% of U.S. households.

I know I am simplifying here. Even with many agreed upon temporary fixes, longer-term solutions must be found. But lawmakers could still salvage strong economic benefits by avoiding the worst of the cliff’s impacts in the short-term while resolving longer-term issues in the first-half of 2013. Such a “grand bargain” would both increase business and consumer confidence and set the nation on a more sustainable budgetary and debt path that would quickly overcome any of the short-term negative impacts resulting from necessary spending cuts and revenue increases.