My penance (and your burden) for being an absent blogger over the past week or so is a longer post with extra graphics today.

A lot of people, including me, are accustomed to assessing the overall skill level of a state’s or a region’s workforce (and thus its potential to capture growing industries that rely on more highly educated workers) based largely on the percentage of the workforce with a college degree. It is simple, intuitive, and more than a little lazy. It is also becoming a less useful indicator of the supply of labor that is in demand by businesses. Populations with higher levels of educational attainment confer a lot of benefits on a state or region but today, having a high percentage of a state’s or region’s population with at least a BA degree probably says as much about the state’s political and cultural sensibilities (as well is its “demand” for services rather than its “need” for services but that is another post) than it does about its economic performance and potential.

The sense of self-satisfaction we in New England and in New Hampshire enjoy about having a population with among the highest levels of educational attainment in the country is palpable, but the reality is that more states are increasing their levels of educational attainment and New England and the Northeast stand-out far less than in the past. Moreover, in an economy that is increasingly rewarding particular skills and degrees more than just high educational attainment, it is not as clear that much of the region still has an edge on the one resource that it has that is always in demand – talent.

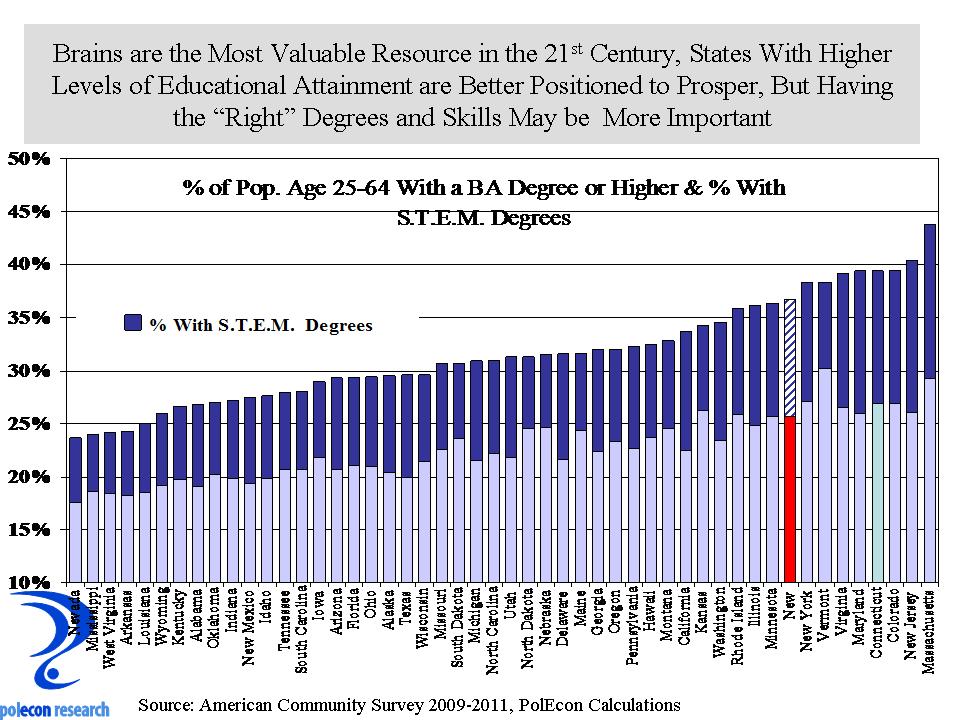

Much of New England and the Northeast has a high percentage of its adult population with a four-year college degree or higher (see chart below).

Just looking at levels of educational attainment tells only part of the story. I can’t blog for too long without talking about the “skills-gap” so here goes. Much of the demand for college-trained labor is in fields that require scientific, technical, engineering, or mathematical (STEM) skills and degrees. The percentage of a state’s population with a BA or higher degree tells a lot about the availability of STEM skills but for a number of states it tells a lot less. I calculated the percentage of a state’s population with a STEM degree (based on first college degree earned) and included it above as the dark blue portion of the bar graph. The official listing of STEM fields is maintained, surprisingly, by the Dept. of Homeland Security ( I categorized 171 college degrees into STEM and non-STEM degrees and I think my listing is close but not a perfect match). If you compare the percentage of the population with a four-year or higher STEM degree (chart below) with the percentage of the population with a BA degree or higher (chart above) it shows a large change in the relative rankings of a number of states, and a some in New England in particular.

The final chart makes just that comparison, it shows the change in ranking between a state’s position on the percentage of its adult working population with at least a BA degree and the percentage of its population with a STEM degree. The chart highlights states that may be over and underrated on the skill level (at least skills in demand) of their workforce. Vermont stands out as having the biggest drop in rankings between the percentage of its population with at least a BA degree and its ranking on the percentage of the population with a STEM degree. Maine also fares poorly. But New Hampshire, Rhode Island, and Connecticut also drop in rankings when measuring “talent in-demand” among the workforce. Only Massachusetts does not drop in ranking ( it is ranked number one on both measures so there is no way it could show anything but a drop in relative rankings). On the other hand, states that are often derided by Northeastern “elites”, such as Texas, Arizona, Florida and Alabama have a smaller percentage of college-trained labor but more of them (on a percentage basis) are trained in the STEM fields most in demand. Still, they don’t have as high a percentage of their adult populations with a STEM degree as do some New England and some other states, but with population and migration trends, and as more individuals with those skills and more companies that want access to them agglomerate in those states, how long before some take the lead in “talent”? I don’t think Massachusetts has as much to worry about as do other states in New England because of their unique higher-education assets. The question for the rest of us is, can we continue to “beggar our neighbor” and benefit from the Bay State’s ability to churn-out and attract individuals with the degrees and skills in demand?

As New Jersey, New York, and Connecticut show, having a lot of “talent” in your workforce doesn’t guarantee strong economic growth. The business, political, environmental, and even cultural and social climates also play an important role in promoting prosperity. I look at states with a relatively higher percentage of their college trained workforces in STEM fields as “up-and-comers.” Most don’t have the history of high educational attainment in their populations that New England does, so their overall ranking on educational attainment tends to be lower. Some, like Texas and Arizona also have had a large influx of individuals with traditionally lower levels of educational attainment. Nevertheless, they are accumulating and growing a larger portion of the nation’s “talent” in STEM fields and over the long-haul, that is the biggest threat to New England’s most valuable and most in-demand resource, and thus the biggest threat to its prosperity.