Low interest rates did much to float the housing bubble of the 2000s, but like all bubbles the higher pressure inside the bubble eventually caused it to burst as it rose higher and encountered the thinner atmosphere at high elevations. Recently, even lower interest rates (lower than those that helped create the bubble) have significantly helped the housing recovery .

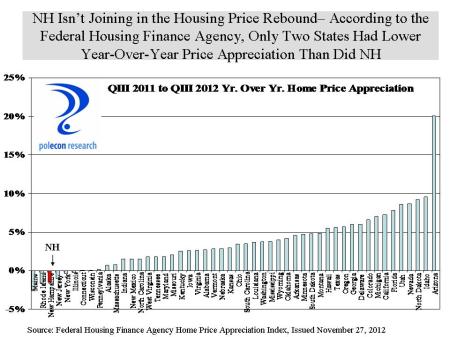

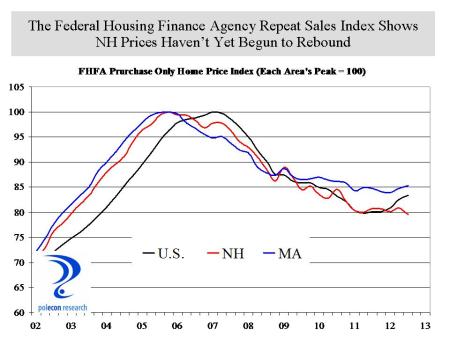

I haven’t written about the housing market lately because you can only jump off the “booming housing market” bandwagon so many times before people start wishing it causes you a fatal injury. I won’t jump off the housing recovery bandwagon this post so much as I will move to the back of the wagon. There is a nice modest recovery occurring in New Hampshire’s housing market. It is not the boom that some national headlines indicate, or even as strong as some data on median sales prices in New Hampshire would suggest, but the market is recovering. CoreLogic’s home price indices show New Hampshire prices appreciated at about 5% over the past year. Not bad but still 30 states had greater home price appreciation. Home prices in the Granite state remain almost 17% below their peak levels and in only 12 states to prices remain further below their peak levels.

Population growth (largely through in-migration) appears to be resuming again in New Hampshire and as household formations and job growth accelerate the market should improve at a faster rate. Housing affordability is as high as it has been in decades. The chart below shows a housing affordability index, or how the monthly income of a NH household at the median income in the state relates to the monthly principal and interest costs of buying a home at the median price in the state. When the index is above one, the index shows that the “typical” household with income at the state median, has more than enough income to cover monthly principal and interest costs (it says nothing about whether they have enough to make a 10 or 20% down payment to make the purchase or the ability to qualify for a mortgage). The chart also shows how affordability changes at higher interest rates, indicating that for every 1% rise in mortgage interest rates, affordability declines by about 10%.

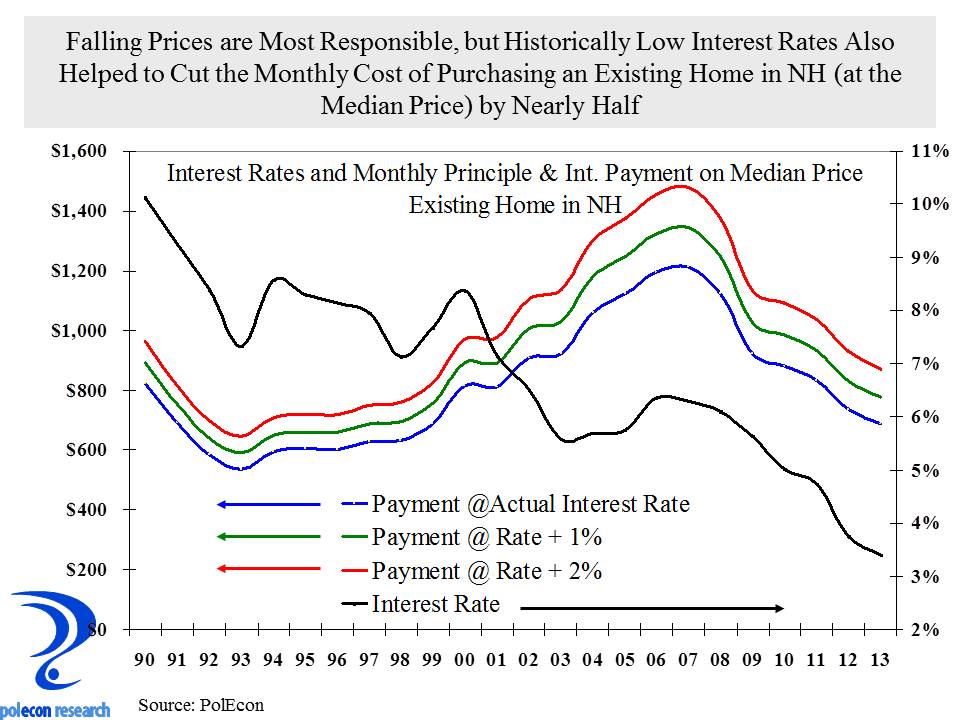

The final chart shows how dramatically the combination of lower prices and falling interest rates affects the monthly principal and interest payments required to purchase a home in New Hampshire at the median purchase price and prevailing interest rates. The chart also shows how the monthly principal and interest payments on a median priced home in NH would have been affected by interest rates that were 1% and 2% higher than they actually were. The chart shows how significant changes in monthly payments can be at higher interest rates. The impact of interest rates on monthly payments is more dramatic when home prices are higher so lower prices in this case suggest that an uptick in rates may have somewhat less of an impact than in the past. Nevertheless the impact on affordability and prices of higher interest rates will be clear.

A key question is how much of the recent rise in prices is the result of a genuine increase in effective demand for homes and how much is the result of the capitalization of interest rates into the purchase price (when rates are low sellers can get higher prices and still keep housing affordable but when mortgage rates are higher sellers must charge less to keep the same level of affordability). For certain we know that more homes are being purchased, what we will find out, if interest rates continue to rise, is how much of that and sales prices are driven by low interest rates. In new Hampshire this is especially critical because we have a relatively high percentage of homeowners with negative or near negative equity in their homes and changes in interest rates may determine whether or not they can sell their homes without incurring a loss.