Archive for November 2012

November 30, 2012

Households are arguably better positioned to increase their spending than at any time over the past decade. I define household purchasing power, in the aggregate, as a combination of income and household financial obligations. Household financial obligations include all debt obligations as well as things like housing rental costs, auto leases, insurance and property tax payments. A combination of low interest rates that reduce the cost of debt for households as well as reductions in the use of credit and households paying down debt since the recession, have all combined to lower the financial obligations of households (in the aggregate) as a percentage of household disposable income. Real wage and salary income is also increasing (even if not for all individual households). In combination, the reduction in financial obligations and rising aggregate income should result in increasing consumer expenditures. A lack of conviction in the economic recovery, a decline in home values that affect consumer’s sense of financial well-being, and higher energy prices over the past year have all helped restrain consumer confidence and spending. But energy prices are falling and home prices (in most areas) are rising. As hiring (and thus wage and salary growth) accelerates, the stage is set for a long-awaited burst of consumer spending.

Categories: consumers, Debt, Financial, Household Finances

Tags: Consumer spending, consumers, debt, financial obligations, households, purchasing power

Comments: Be the first to comment

November 29, 2012

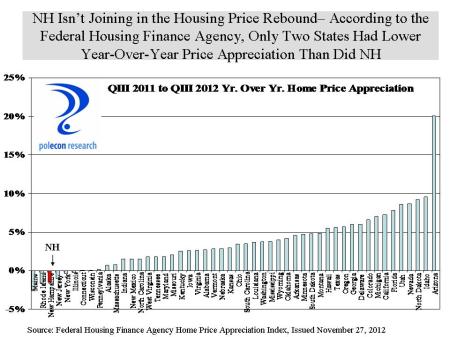

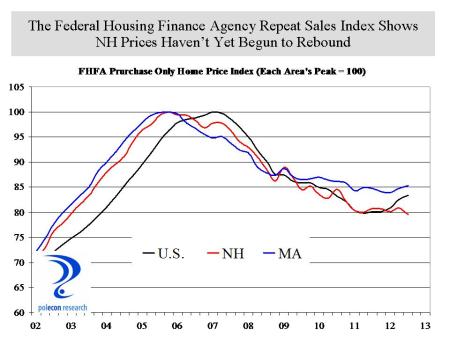

The Federal Housing Finance Agency released its latest home price appreciation index on Tuesday and while the data support the belief that housing is bouncing back across the country, and is now becoming a positive influence on economic activity rather than a drag, the news is not good for New Hampshire. The FHFA’ s repeat sales home price index shows that NH is one of only a few states that had price depreciation between the third quarter of 2011 and the third quarter of 2012 and only two states (Maine and Rhodes Island) had lower appreciation rates than did New Hampshire.

Repeat sales indices are the only accurate way to measure changes in home prices. Simply examining median sales prices doesn’t account for the fact that the characteristics of the houses sold may be different (location, size, type, etc.) unless the repeat sales method is used. I am by nature an optimist. I am rooting for the housing market because its rebound is important for the prospects of the NH economy and its not so bad for my balance sheet either. I am also not looking for yet another reason for realtors to take exception to some of my analyses. I am, however, a believer in the wisdom of markets (most of the time) but a lot of what happens in markets is driven by pure stupidity – or, rather, inattention, misinformation about fundamentals, and an exaggerated focus on currently circulating stories (the housing market is back, Mitt Romney has got the momentum in the swing states). At least one of those stories is true , the housing market is coming back as a whole in the nation, just not everywhere.

As I have noted in prior posts, no amount of exhortation and cheer leading about housing can overcome the fact that values are determined by fundamental underlying demand for housing which includes population and job growth, the formation of new households, and the need to replace older housing units. Both NH’s job and population growth have been weak relative to a majority of states over the past couple of years. Regressing job and population growth over the past year in each state on the FHFA’s home price index-based change in home prices in each state shows a highly significant relationship (R=.603) accounting for about 40 percent of the variation in home price appreciation across states. There are variations in markets within each state, and this analysis is an oversimplification, but nevertheless it is important to remember that home price appreciation cannot, for long at least, outpace the fundamental determinants of the demand for housing – job, population and household formation growth, and the need to replace obsolete structures.

Categories: House Prices, Housing, Real Estate

Tags: appreciation, home prices, home sales, Housing, job growth, NH, population growth

Comments: 2 Comments

November 28, 2012

Small businesses fared the worst during the recent recession and hiring by small businesses has been slower to recover after this recession than it was following past recessions. Robust economic growth does not occur unless small businesses are confident, healthy, and hiring. With a fragile national recovery from recession that has not quickly helped to repair the balance sheets of most small businesses, and with a number of important public policies (regulatory, tax, health care etc.) still uncertain, it is not surprising that small businesses have been less than sanguine about the prospects for the economy and reluctant to hire. That may be changing, however, as the NFIB’s national index of small business optimism has begun to increase. The NFIB index is a pretty good predictor of the direction of job growth in NH and its latest up-tick is consistent with last month’s increase in payroll employment in New Hampshire.

Categories: job growth, NH Economy, Small Business

Tags: employment growth, NFIB, NH, optimism, Small businesses

Comments: Be the first to comment

November 27, 2012

Linguists will take exception to that and note that a cliff is, in fact, a bluff. The consensus among economists, however, is that the fiscal cliff is indeed no bluff. A number of commentators have noted that the fiscal cliff is more like a slope and will not cause immediate economic calamity. I was one of those as a guest on NHPR’s “The Exchange“. But just as there was once too much hyperbole surrounding the fiscal cliff issue, now, as we get closer to the deadlines when the combination of tax hikes and spending cuts that define the fiscal cliff take effect, there seems to be more of an effort to minimize the likely impacts that will occur if no resolution is found. That would be a mistake because whether the spending cuts take effect immediately or over the course of a year or more, and whether the tax hikes immediately effect spending and investment decisions is not the issue. The issue is that the U.S. economy is simply not growing fast enough to withstand the impacts of the full implementation of the provisions of the fiscal cliff. Skeptics fire away, but below is a succinct chart that shows how the effects of the fiscal cliff relate to real growth in our nation’s economy, assuming the effects of the cliff occur in 2014. To lump all effects in one year isn’t accurate, but the point is to place the magnitude of the cliff’s impacts into context. I believe the context in the chart below highlights the importance of a reasonable resolution to the potential problems the cliff could cause.

Categories: Fiscal Cliff, Fiscal Policy, Politics

Tags: fiscal cliff, GDP, growth, impacts, recession

Comments: 1 Comment

November 26, 2012

I started this analysis wondering if the percentage of jobs in professional, technical, and scientific industries in NH that are held by females is greater among younger workers in the industry than older workers. I became sidetracked by the unexpected finding that the percentage of workers in those industries is about evenly divided between men and women (and as a spoiler the percentage that is female is larger at younger age groups – consistent with my “‘feminization of the NH workforce” theme from an earlier post). One caveat before proclaiming gender equity in professional and scientific fields, the data do not account for the specific occupations in the industries. That is, it is possible that the conventional wisdom that women are less employed in those industries is not supported, but the fact may remain that the more professional, scientific, and technical occupations in those industries (as opposed to the management, support and other occupations) may still be dominated by males. Unfortunately there is data from different datasets that supports this thesis, although it does appear to be changing.

The chart below shows that women comprise about half of the employment in the broad industry grouping of professional, scientific, and technical industries.

The real kicker in the data is that it shows that reductions in employment in those industries came largely at the expense of female workers. Again, this may just be a function of the reductions in those industries occurring in specific occupations more likely to be populated by females, a viable interpretation. It may also be related to an increase in female employment among younger and newer workers in the industry who’s employment may be most vulnerable in a recession. Nevertheless, such a high percentage of decline in those industries coming at the expense of female workers is well beyond what would be expected based on probability and chance alone.

Categories: Gender, Unemployment

Tags: female, job growth, NH, professional, recession, scientific, technical, unemployment, workforce

Comments: 1 Comment

November 21, 2012

A quick review: The “skills gap” explanation for slower employment growth this recovery posits that there are large numbers of jobs waiting to be filled but hiring is sub-par after the recession because of a lack of qualified candidates to fill those positions. Twice I have presented some evidence on the issue, here and here. Most of the concern and evidence about the existence of a skills gap addresses very high-skill technical, scientific, computer, and engineering occupations because our nation, and by extension our state, seem to perpetually be unable to produce enough individuals in those fields to satisfy industry demand. As a result we “import” a lot of that talent from foreign countries (more about this – I promise – in a future post). There is some evidence of this in NH. As the chart below shows, professional, scientific, and technology occupations are the largest, broad category of help wanted ads in the state. But they have also evidenced the smallest increase (a decrease actually) since the recession. There is still a significant demand but it may be that an inability to find qualified applicants has companies in need of those occupations from considering more hiring in the Granite State. A quick review of data for Massachusetts shows that demand for professional, scientific and technical occupations has increased during the same time period.

But more direct evidence of a skills gap comes from the demand for construction and production workers. I am especially interested in the potential skills gap for production workers. The chart above shows that demand for construction, production, and transportation workers has increased significantly since the recession. Although still a much smaller category of help-wanted ads than professional and technical jobs, the increased demand is consistent with anecdotal evidence I heard this week at a roundtable discussion of the Seacoast economy. At that discussion, representatives from industry, higher education, and economic development organizations cited specific examples of companies frustrated at their ability to hire skilled production workers. Some are forming partnerships with NH’s community college system to increase the supply of needed occupations. Those initiatives show promise and I hope the state’s four-year colleges and universities develop more partnerships to address the skills gap in professional, scientific and technical occupations as well because, increasingly, job growth in NH appears to depend on it.

Categories: Help Wanted, job growth, NH Economy, Skills Gap

Tags: help-wanted, job growth, NH, occupation, occupational demand, Skills gap

Comments: 1 Comment

November 20, 2012

The U.S. Bureau of Labor Statistics released its monthly report on state and local employment today and the good news is that, preliminarily, New Hampshire added 1,000 jobs in October. The bad news is that this is just 1,200 more jobs than the state had one year earlier in October of 2011. For optimists, the most recent trend is likely to be the most important and the monthly report is consistent with the rise in PolEcon’s NH Leading Index.

Nevertheless, the longer-term job growth trend in NH has been weak. Looking at growth in just private sector employment, the situation is no better for NH. As I have noted here, I believe job growth in NH is being underestimated but even if that is true, it is hard to see how the recent past will be revised enough to make NH’s job growth picture look comparable to that of our neighbor to the south or the U.S. as a whole.

Categories: job growth, NH Economy, U,S, Economy

Tags: employment, employment growth, job growth, jobs, NH

Comments: 2 Comments

November 19, 2012

The rise in natural gas production in the U.S., along with the volume of proved reserves available in the future because of new technologies, could fundamentally change the energy landscape in the U.S. in a way that the significant and beneficial rise in U.S. oil production can not. Both trends are good news for the country and further efforts toward U.S. energy independence, but the lower prices and increased stability in supply of natural gas also have the potential to alter the energy fuel mix in this country. The use of natural gas has yet to make significant inroads in the transportation sector but it is hard to imagine how a fuel supply that (unlike gasoline) is, or could be, available directly at a majority of U.S. households at reasonable prices, will not eventually fuel a much higher percentage of vehicles in this country. In the electric power industry, the transition to natural gas is already occurring, in part because of the lower and more stable price environment for natural gas, but also because of the environmental advantages of natural gas.

The chart above shows that the price of natural gas used by the electric power industry for generation has fallen by almost 60 percent since 2005. Although that trend will not continue, production and proved reserves in the U.S. have created a much more predictable and stable price environment for natural gas as evidenced by forecasts by the U.S. Energy Information Agency and by commodity futures markets. The electric power industry is already changing to reflect the new realities of natural gas markets. As the chart below shows, in just the past decade electricity generated using natural gas has gone from 15 percent of the electricity generated by coal fired power plants to 31 percent.

That trend is continuing. Just one company (First Energy), recently announced the closing of six coal fired power plants in Ohio, Michigan, Pennsylvania, and Maryland, noting that the costs of environmental compliance upgrades made the plants not economically viable to continue to operate.

Categories: Electricity Generation, Energy, Natural Gas, Uncategorized

Tags: coal, electric power, electricity generation, Energy, Natural Gas, NH

Comments: 1 Comment

November 16, 2012

The rate of home ownership increased significantly in the U.S. and in New Hampshire from the middle of the 1990’s until the housing market crash in the late 2000s. The increased availability of financing (sometimes exotic) played a significant role, as it did in the ultimate unwinding of the housing boom (nearly taking the nation’s financial system down along the way). Home ownership rates are returning to levels closer to historical standards in the U.S., but not before a lot of household wealth in the form of homeowners equity was lost. That has had a large impact on our recovery from recession. One rule of thumb is that for every one dollar of household net worth lost, consumption expenditures by households will decline by 3-5 cents (the so called “wealth-effect”. Using the lower figure (3 cents), implies that across the country, consumer expenditures were about $180 billion lower between 2007 and 2011 as a result of the housing market crash, than they would have otherwise have been.

In NH, home ownership rates are higher than for the U.S. and they have yet to significantly move back toward their historical levels in the state. They may never, but I have to think that until they do, putting a true value on houses in the state is going to be difficult. In the meantime, home price depreciation has had the same negative effect on household net worth in the Granite State and thus a substantial negative impact on consumer expenditures via the “wealth-effect”.

Categories: Homeownership, Household Finances, Housing, Real Estate

Tags: financial crisis, homeownership, homeownership rates, housing market, housing market bust, NH

Comments: Be the first to comment

November 15, 2012

The Consumer Distress Index is a quarterly comprehensive picture of the average American household’s financial condition. The index is calculated for the nation and each of the 50 states. The index measures 5 categories of personal finance that reflect or lead to a secure, stable financial life—Employment, Housing, Credit, Household Budget and Net Worth. It is calculated by CredAbility, a nonprofit credit counseling service, uses 65 data points using public and private data to measure consumer financial distress. According to their Consumer Distress Index, only 12 states have lower levels of financial distress among households than does New Hampshire. Lower scores indicate higher levels of financial distress. The chart below compares NH with the U.S. average. It shows that, by this measure, NH households are about as financially well-off as they were just prior to the recession, but that the financial health of households has generally deteriorated since the second-half of the last decade. Not surprising given the increases in employment insecurity and decreases in the value of most households largest asset, their home.

CredAbility categorizes distress scores using the following:

Less than 60 Emergency / Crisis

60 – 69 Distressed / Unstable

70 – 79 Weakening / At-Risk

80 – 89 Good / Stable

90 and Above Excellent / Secure

By that scale NH, with a score of 75.68 is “At-Risk”, while the U.S. average household is bordering on “unstable/distressed” with a score of 70.48. According to this measure, NH households are about or just slightly below where they were prior to the recession in terms of financial distress, while the average U.S. household is in more financial distress than they were prior to the recession. I don’t know how much concurrent validity this measure has but I do know that if I had used it, instead of a state-level “misery index” (the sum of unemployment and inflation) to predict the outcome of the election it would have been a less accurate predictor of election results.

Categories: consumers, Financial, Household Finances

Tags: consumer distress, consumer finances, consumers, financial distress

Comments: Be the first to comment