In July, the current U.S. economic expansion will become the longest on record and there have been a record 103 consecutive months of uninterrupted job growth. Not counting the distorting effects of the hiring (and then letting go) of over 411,000 temporary workers on the U.S. Census back in 2009-2010 it would have been 110 consecutive months of job growth. A similar effect will occur in 2019 and 2020 as the Census Bureau begins hiring temporary Census workers this year and will lay off the workers later in 2020. You can look forward to a lot of misinterpretation of the job growth numbers in the presidential election year of 2020.

The U.S. economy is strong, but as I argued in my previous post, not as strong as the first estimate of QI GDP growth (3.2%) suggests. In that post I noted the one-off contributors (inventory builds, lower imports, higher defense spending) to above potential GDP in the first quarter of 2019. In this post I highlight two employment trends that indicate (to me at least) the U.S. economy is not growing as rapidly as recent reports suggest.

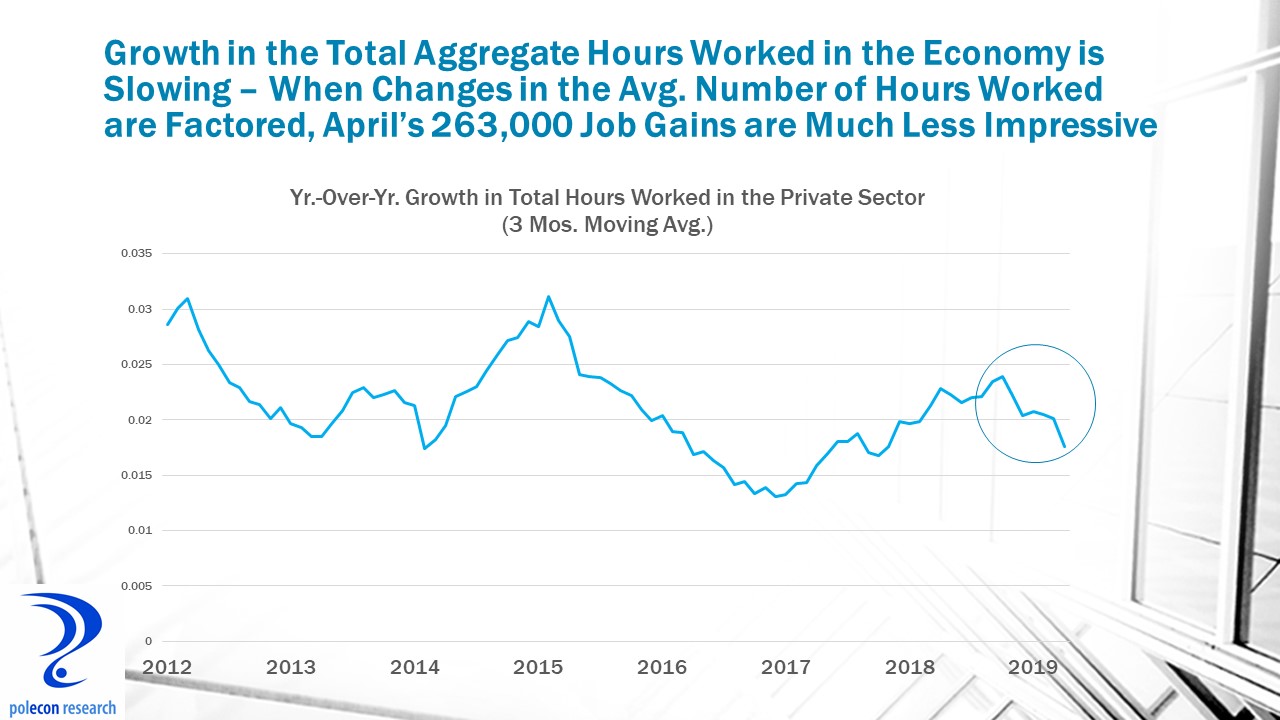

First, growth in aggregate hours worked in the economy is slowing, despite strong gains in job growth. Aggregate hours worked is a function of both job growth and the number of hours worked each week and the latter has shrunk a bit, offsetting some of the gains in employment. Aggregate hours worked is related to GDP growth because the more hours worked, the more output the U.S. economy produces.

The growth in aggregate hours worked plus productivity growth is a good surrogate measure of trends in GDP growth. Growth in aggregate hours worked plus growth in productivity (how much each worker produces), at a minimum, will tell you whether GDP growth is accelerating or decelerating. When the average number of hours worked each week is factored into job growth, April job growth looks much more like 100,000 or less, than 263,000. This makes sense because productivity growth in the first quarter was initially estimated at 3.4%, a remarkably high rate given that annual productivity growth has averaged about 1% for a decade and the combination of 263,000 job growth and 3.4% productivity growth would imply a very high GDP growth (higher than the 3.2% first quarter growth first reported but which I believe will be revised downward). Productivity growth is notoriously difficult to calculate and count me skeptical of the 3.4% estimate for the first quarter. Still, the first estimate is the one that gets the headlines and later revisions garner less attention.

The rate of job growth is also slowing, not accelerating, as the initial April job growth estimate implies. Again, the labor market is strong, there are more job openings than workers available to fill them. Both of the survey instruments used to measure employment tell a similar story of job growth that is solid but slowing. Briefly, the payroll survey is a survey of employers in the country, it provides an estimate of the number of non-farm jobs, the average number of hours worked by employees, and the average hourly wages that they are paid. The payroll survey does not count the self-employed or those not covered by the unemployment insurance program. It also counts jobs, not people, so one employed person holding two jobs is counted as two jobs by the survey. The household survey is used to calculate the unemployment rate and labor force participation. It provides much more information about the characteristics of the employed and of job growth or job loss in a month than does the payroll (employer) survey. The household survey counts the self-employed and those not covered by unemployment insurance and it counts an individual working more than one job as a single job for total employment purposes.

The household survey tends to be more volatile, as can be seen in the chart above, but the relevant point is that both surveys show employment growth slowing. That does not necessarily mean a weaker U.S. economy, but rather than the economy is unable to growth because of labor constraints. The monthly Job Growth and Labor Turnover Survey (JOLTS) highlights this fact. Looking at the JOLTS data released today shows that the job openings rate continues to rise much faster than the hiring rate, highlighting the growing gap between labor demand and labor supply. The chart below shows how the gap between openings and hires has grown in just the Northeast region of the country, where labor shortages are among the most acute.

In conclusion, the U.S. economy is solid and labor markets are strong, just not as strong as recent data points suggest, and at a time when there are more downside than upside risks to the outlook.