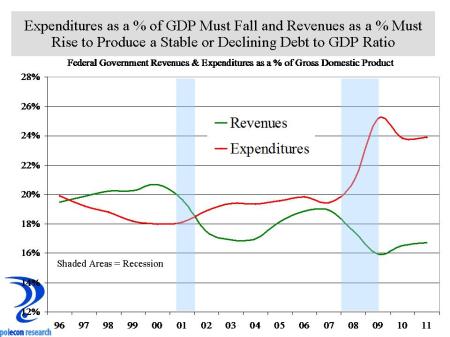

Federal government revenues as a percentage of gross domestic product have averaged about 18% over the past 50 years (the median is also 18%). Federal government revenue is “pro-cyclical,” that means revenues as a percentage of GDP grow when the economy is stronger, as profitability of businesses increases and as individual wage, salary and investment income is increasing. This relationship has a couple of important implications: First, it can confound ideological interpretations of the appropriate level of current revenues as a percentage of the economy because higher revenues as a percentage of GDP aren’t associated with slow growth and low percentages aren’t associated with higher rates of economic growth – just the opposite is true (with the exception of the dual recessions of the early 1980s), second it suggests how important economic growth is to revenue growth and thus to potentially reducing the nation’s budget deficit.

I haven’t done the math but others who have indicate that the various deficit reduction proposals all require revenues as a percentage of GDP of over 18%. The U.S. House passed Ryan budget proposal would produce estimated revenues as a percentage of forecast GDP of approximately 19%, the President’s proposals would produce estimated revenues at 20% of GDP, and the “Simpson-Bowles” model would result in estimated revenues as a percentage of forecast GDP of 21%. That doesn’t sound like much of a difference, but in an economy with a GDP of $15.5 trillion each 1% increase equates to $155 billion in revenue. Going from federal revenues that are 18% of GDP to 21% implies a revenue increase of $465 billion. I could be ok with that if the bulk of the increase were the result of a roaring economy producing large increases in profitability and income, but that isn’t the foundation of any deficit reduction plan and it is hard to see a scenario where $465 of additional revenue is consistent with a high growth economy (the pro-cyclical nature of revenues aside – that relationship isn’t infinitely linear). The national debate over reducing our nation’s budget deficit is framed by two choices or their combinations, increasing tax rates (or eliminating temporary reductions and reducing tax breaks etc.) or by cutting spending. Revenues at 18% of GDP seems to have worked reasonably well over the past one-half century with the past decade being the exception. It may be time to aim for a different ratio for the sake of longer-term fiscal balance, but I wouldn’t do it without first exhausting opportunities for spending reductions that maintain a ratio close to the historical average of 18%. But whatever the combination of spending reductions and revenue increases that eventually becomes the strategy for addressing the nation’s long-term fiscal imbalances, I hope economic growth is the ultimate goal, because as the chart above shows, achieving that goal will make addressing fiscal imbalances a much more manageable task.