On only a few issues can I say that I would be happy to be wrong. My views on likely home price appreciation and New Hampshire’s housing market is one of them. Housing is important to the state’s economic recovery and longer-term prospects for economic growth. By way of shameless self-promotion, I will be on NH Public Radio’s “The Exchange” discussing some of my views on the topic. I’m not a real estate economist so it will be interesting to hear how my views differ from someone who will also be a guest and who is a very good real estate economist, (Russ Thibeault from Applied Economic Research).

The problem I have with most discussions of the housing market is that housing is by far the economic metric that individuals have the most emotional, psychological and often direct financial attachment to. Discussions of the housing market are the most prone to hope, optimism, and wishful thinking, and the least amenable (and welcome) to dispassionate analysis. If you want something to be true it is as easy to find evidence to support your view as it is to dismiss evidence that contradicts it. Every day we hear about the housing comeback nationally so we want to believe it is happening in NH, and we will look for any sign that it is. I don’t see much evidence that the housing market is recovering as fast in NH as it is nationally and I don’t see factors in the near future that will contribute to it being so. Long term, job and population growth are the best determinants of home price appreciation in a region and neither bodes well for a quick housing comeback in NH. The chart below shows the relationship between year-over-year home price appreciation in each state and job growth during the same time period. Each marker represents one state’s value on job growth (the horizontal or “x” axis) and its rate of home price appreciation over the same time period (the vertical or “y” axis). Some states with large price declines are seeing out-sized rebounds but job and population growth largely determine price appreciation trends over the long-term (during bubble times that relationship breaks down but eventually it returns to trend), NH is the red marker and reflects a state with both low job growth and appreciation rates over the past year.

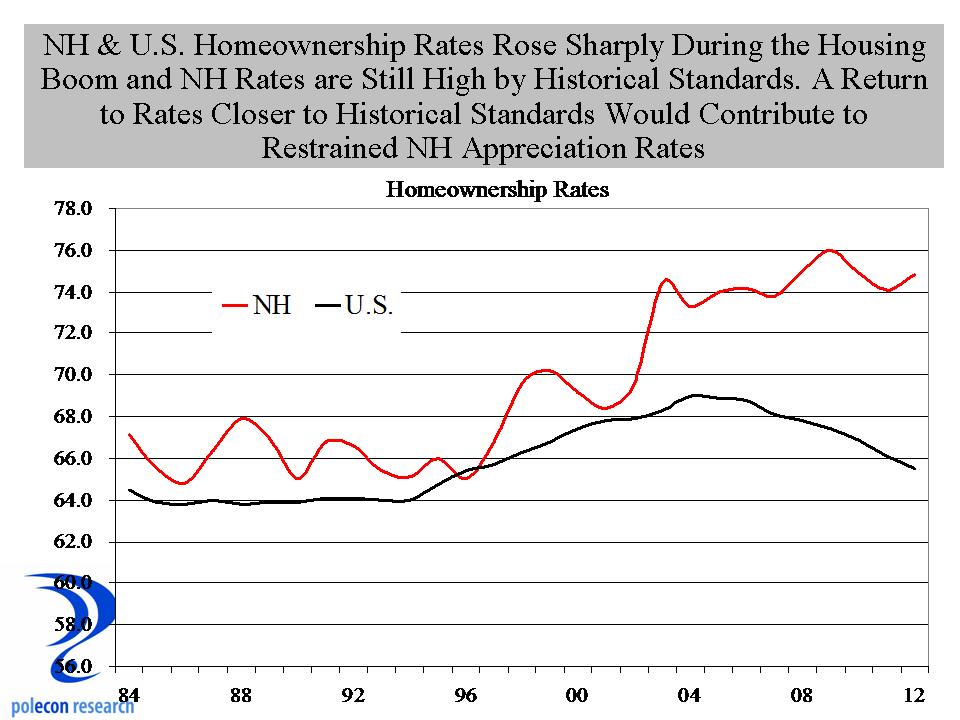

I know home sales have increased significantly in NH over the past year but I wonder how large a role investor purchases for conversion to rental housing is playing in that trend. For a number of reasons, that I will discuss in future posts, I think economic, demographic, financial, socioeconomic and social trends are likely to favor the performance of rental housing relative to homeownership in NH for several years. Nationally and in almost all states, the homeownership rate fell during the housing market crash. NH has a high homeownership rate and it barely dropped during the crash. Many states are seeing homeownership rates begin to rebound and will see demand and price appreciation benefits from that. Meanwhile, NH’s rate remains at historically high levels and given the demographic and other trends I don’t have time to discuss in this post, I think the rate will move lower and closer to the state’s long-term rates. That won’t help price appreciation.

Gosh that sounds apocalyptic, its not, it just means that we shouldn’t soon expect the big price rebounds seen in many states. Except I know we will expect exactly that, because residential real estate is about psychology and about comparables and comparisons, what has happened in the past. Any industry strongly influenced by those factors is going to regularly disappoint.