Improvements in the balance sheets and cash flow of households along with continued if not robust improvement in the labor market bode well for consumer spending as the year progresses, helping the economy overcome the negative impacts of payroll and other tax increases.

Home equity is a strong driver of the buying power and spending decisions of households. Home prices are rebounding across the country and even New Hampshire is beginning to show some strengthening according to Core Logic’s Home Price Appreciation Index. Appreciation in NH remains below a majority of states and well below the 15% suggested by the industry in the state.

While home prices are still off from their 2006 peak, the rise in home prices has raised homeowners’ equity $1.6 trillion over the past year. This is the second largest nominal gain on record since 2005 when homeowners’ equity was up $2.0 trillion. In percentage terms, owners’ equity as a share of household real estate rose to 46.6% last year compared to 40.5% in 2011—the previous cyclical peak was 59.6% in 2005—and an all-time record low of 37.3% in 2009.

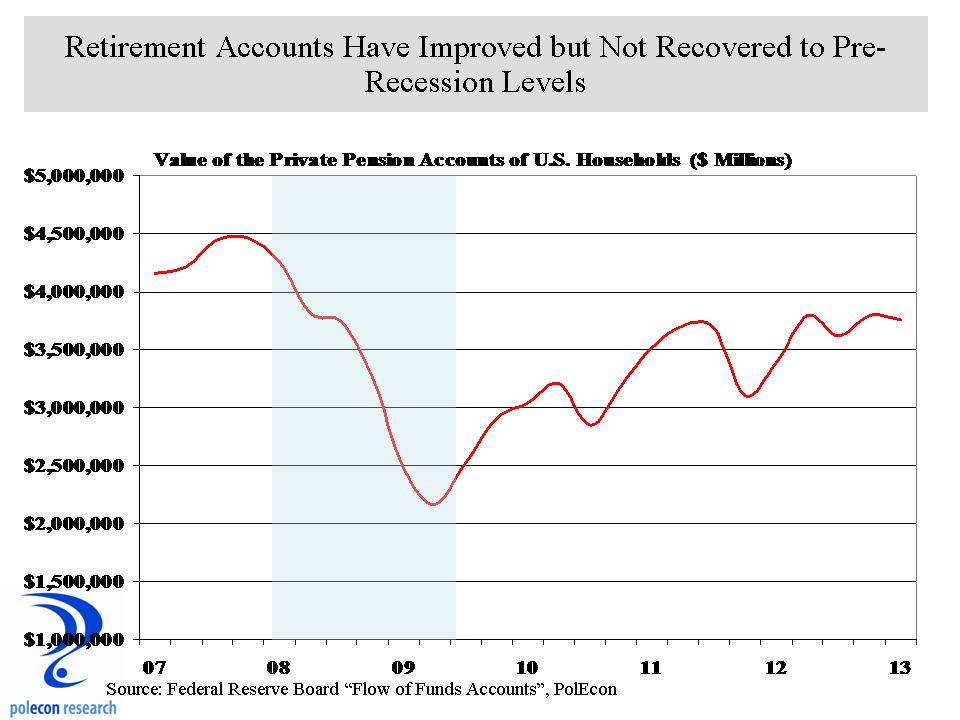

Private retirement and pension accounts represent a much smaller component of the net worth of households but they are key contributor to households’ sense of financial “well-being” and a contributor to the “wealth effect” that impacts household confidence and their willingness to spend.

The equity of homeowners is the largest contributor to the improvement in household net worth but the value of the private pension accounts of households along with the rise in the value of the stock market are adding to consumer’s willingness to spend. Lower interest rates, lower levels of debt, and improvements in wage and salary income are also improving the cash flow of households. In combination, the outlook for consumer buying power and spending in 2013 looks like it could be stronger than the growth in the underlying economy would suggest.