For the calendar year 2018, federal corporate tax revenues were about $91.4 billion lower than during calendar year 2017, a decline of about 32%. The federal corp. tax cuts that took effect in 2018 lowered the tax rate from 35% to 21% and are the primary reason that federal revenues were 0.4% lower in calendar year 2018 compared to 2017 (in a strong economy). All banks are required to file detailed financial reports to regulators on a quarterly basis. Examining that data provides an estimate of how banks were affected by the recent federal tax cuts. Comparing the average effective tax rate of banks between 2013 and 2016 (in 2017 banks paid an an anomalously high rate) to the rate in 2018 and applying the difference to the pretax income of banks provides an estimate of the savings banks received from the corp. tax cut. The table below shows that collectively, banks accounted for $31.7 billion or about 1/3rd of the total corp. tax cut savings, with the 9 largest banks saving almost $15 billion or 16% of the total corporate tax savings in 2018 – an average $1.64 billion per bank. I expect banks, and big banks in particular to have an issue with this estimate so I encourage them to point out errors in my simple methodology.

Posted tagged ‘banks’

Big Banks Big Tax Savings

April 2, 2019It’s a Good Time to Be a Bank

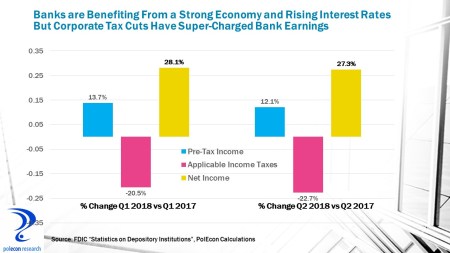

October 15, 2018It’s a good time to be a bank, well a BIG bank anyway. Bank of America’s Q3 profits are up by 32%, JPMorgan/Chase’s by 24%, Wells Fargo by 32% in the 3rd quarter. Higher interest rates, a strong economy and needed (for smaller banks) regulatory relief have helped but the biggest contributor has been the reduction in the corporate tax rate. Industry-wide Q3 results have not yet been reported but looking at Q2 and Q1 2018 data compared to 2017 shows the impact of tax cuts. While banks pre-tax income was up by 12-13% in 2018, net income was up 27-28% because applicable income taxes (federal & state) were down more than 20%.

The banking industry has been perhaps the biggest beneficiary of the Trump administration’s initiatives. Earlier this year I examined over 400 press releases announcing how companies would be using the proceeds from corporate tax cuts and highlighting employee bonuses, minimum wage hikes, etc. (the releases were remarkable in their similarity as were the benefits accruing to employees – a small percentage but more about that in a future post). Despite banks being only about 1% of all business enterprises thy accounted for just over 30% of the press releases highlighting worker and civic benefits of the tax cut.

The Changing Banking Market

October 23, 2012Public antipathy toward large financial institutions may have been building throughout much of the past decade but it surely peaked during and immediately following the recent recession and the financial crisis that helped precipitate it. One result appears to be a changing market structure for deposits and loans at financial institutions in NH and across the country. The recession in our state was less severe than was the recession of the early 1990’s, and less severe than was the recent recession in many states because of the the overall health and strength of our state’s banking institutions. Nevertheless, one fallout from the financial crisis appears to be a growing market share for credit unions in the state. As the chart below shows, since the recent recession, deposits at credit unions have grown much faster than deposits at NH banks overall. Deposits at NH community banks have grown faster than deposits at all NH banks, suggesting that deposit gains by credit unions have come largely at the expense of large banks in the state, as deposit growth for all NH banks is much lower than the growth among just community banks. Prior to the recession and financial crisis, deposits at NH community banks were growing faster than were deposits at credit unions.

It would be unfortunate if community banking institutions that have had strong commitments and links to their local communities and regional economies are tarred by the actions of institutions from afar. Beyond that, a fundamental change in the market shares for financial services could have significant impacts on the regulation of financial services, on government revenues , and on market shares as the tax exempt status of credit unions contributes to their ability to compete and capture market share. The increased concentration of deposits in the banking industry that occurred during much of the 1980’s and 1990’s may now be occurring among credit unions. As the services credit unions offer and their branching look more and more like those of banks, their ownership and regulatory structure may be the only thing that distinguishes them from banks.