In my economic presentations I often say that I am ‘frequently in error but rarely in doubt.” Still, when in error I admit it, it’s a sign that I am willing to ask myself “why” in order to improve my methodologies. I was wrong when I predicted NH’s job growth would be under 1% in 2018 (it is double that), largely because the labor force was able to grow more than I had forecast (see my previous post on net in-migration to the state). In a letter to Congress over 100 economists asserted that “the macroeconomic feedback generated by the “Tax Cuts and Jobs Act” would be “more than enough to compensate for the static revenue loss,” implying that the bill would be deficit-neutral over time. Federal revenues have a seasonal (monthly) variation, with some months bringing in more revenue than the government spends and vice versa. Comparing similar months over time thus offers some insights into the deficit trends over time and in different economic conditions. As the chart below shows, the November 2018 monthly deficit (the most recent data available) show that during a period of solid economic growth the U.S. ran the highest November monthly deficit in its history.

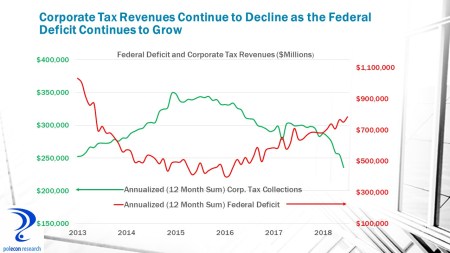

Proponents of the bill also claimed that we would see enough additional investment to boost growth by 4% per year. That implies an increase in annual investment of roughly $800 billion. But, as this post noted, investment has not jumped to that level, nor does it show signs of doing so anytime soon. The economists who predicted that tax cuts would spur a rapid increase in investment and higher revenues have been proven wrong. They have also remained silent, which suggests that they are not at all surprised to see revenues and investment fall far short of what they promised. Many, if not most, will dismiss the rising deficit (see below) during times of solid economic growth as a function of rising spending.

Rising spending is, in fact, a major but not unexpected contributor to the deficit problem. Stagnant or declining revenues in a strong economy are not the norm, and are the kind of pro-cyclical fiscal policy (cutting taxes in a strong economy instead of filling coffers during a strong economy so that taxes can be cut to stimulate the economy when it is weak) that is going to make the next economic downturn much more difficult to combat.