Bad news arrived today with the release of the monthly employment report by the U.S. Bureau of Labor Statistics. Only 88,000 non-farm jobs were added across the country in March. Following two months which saw the U.S. add 148,000 and 268,000 jobs respectively in January and February, the low number raises concerns that the U.S. may again be heading for a “Summer slump” after showing signs of stronger job growth early in the year.

I share that concern but I am most interested in what the job growth numbers may or may not imply about recent U.S. economic and domestic policies. I know sequestration is the hot policy topic and may be blamed or credited for all evil or good that occurs in the U.S, economy this year, but it is really too early for it to register much impact on March’s job growth. Two other policies have the potential to more significantly impact job growth in the near term. The details of the March employment report provide some clues about if and how these policies may affect job growth in the future. The elimination of the temporary reduction in the payroll tax and health care coverage mandates in the Affordable Care Act are policy impacts that we worried about before we started worrying more about the potential impacts of sequestration.

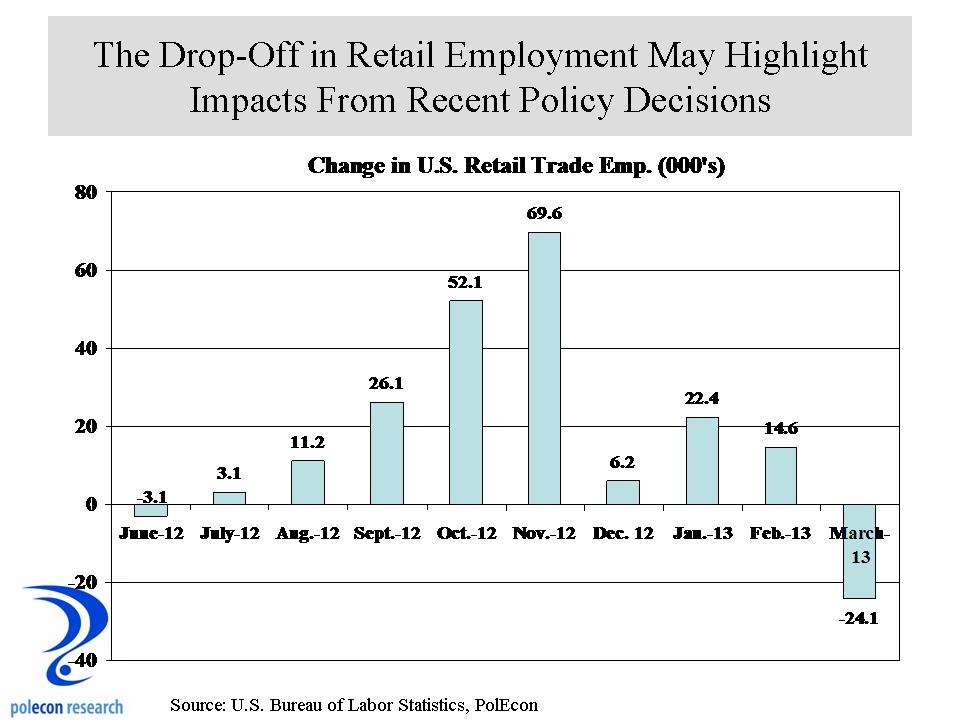

I last posted that gains in home values, stocks and, retirement accounts along with increases in wages and salaries would help the economy overcome the large potential impact on consumer spending from the rise in the payroll tax (elimination of the temporary rate reduction) that took effect in January. I may have been a little too optimistic about those factors ability to help the U.S. economy overcome more than $100 billion in lost consumer spending power (over $600 million in New Hampshire). For me, the most troubling piece of data from the March job growth report was the seasonally adjusted decline of 24 thousand retail trade workers and generally downward trend since January, that has followed several months of solid gains in late 2012 (chart below).

When housing values are recovering, homeowner’s equity is rising, and employment and wages are growing, retail employment should not decline. The elimination of the payroll tax cut (along with higher gasoline prices early in the year) likely provided a greater shock to consumers than anticipated. But another explanation is that implementation of the health care mandates of the ACA could be affecting employment more in some industries. If so, it would likely impact industries that typically are less likely to offer their employees health care coverage and industries that employ more part-time workers. Retail and leisure and hospitality industries meet those criteria but only retail trade lost employment in March. Because the ACA mandates coverage for full-time employees, one way to avoid the mandate would be to increase part-time employment. In that case I would expect the average weekly hours of workers in retail or other industries that may be more affected by the mandate to decline, as more workers were shifted to part-time status but average hours have increased slightly in retail over the past three months. Looking more closely at the data on part-time employment is needed to get a handle on any ACA impacts. Over the next few months I will be looking for evidence of increases in the number of workers working “part-time for economic reasons” – meaning they are working part-time when they want to be working full-time, as well as employment trends in businesses employing between 50 and 499 workers (those most affected by ACA). Trends in these employment data would provide stronger evidence of any ACA effects but for now, it looks like the payroll tax is the culprit in the retail employment data.