What to do about New Hampshire’s business taxes is near the top of lawmaker’s agenda in the Granite State. Many policymakers are concerned that the business tax climate is contributing to a fundamental erosion of New Hampshire’s business climate that is reflected in lackluster employment and revenue growth. Reports that NH has recently outperformed New England and the U.S. in gross state product (GSP) growth highlight the disconnect that can occur between economic metrics of output (GSP) and measures that more directly affect individuals in their daily lives, such as employment and wage growth. Better than regional or national average growth in GSP is good but state-level GSP numbers are relatively imprecise and should not obscure the fact that employment, wages, and state revenue growth have all been disappointing in NH by the standards of the past few decades. Sustained, disappointing employment and revenue growth since the end of the recession have prompted well-meaning lawmakers in NH to consider a number of policies to accelerate growth in the state.

Business Taxes Seen as Key

Business tax rates impact business decisions but I don’t believe they are the fundamental factor behind NH’s disappointing economic performance. Lawmakers should consider “what to do about business taxes” but that consideration should go well beyond current tax rates and regulations. Lawmakers should also be concerned with the long-term prospects (revenue yield) of business taxes because business taxes are the largest source of general revenue supporting state government. New Hampshire’s fiscal structure is fundamentally tied to the performance of the state’s business taxes. As importantly, lawmakers should be concerned with how NH’s business taxes will interact with key economic and demographic trends to influence the state’s future economic performance. The chart below shows combined quarterly business profits and business enterprise tax collections on an annualized basis and illustrates that nearly six years post-recession and more than seven past their high mark, business tax revenues in NH have not fully recovered. Some of the failure of revenues to rebound following the recession is a result of changes in the state’s business tax rules and some is the result of total private sector wages and salaries (the largest portion of the BET tax base) that declined in 2009 and 2010. Whatever the reason it highlights concerns about the viability of business taxes as the primary source of support for state government. I don’t believe that either raising or lowering rates is likely to improve the performance of business tax revenue enough to alleviate those concerns or even result in revenue gains that match those seen in the first half of the 2000s.

The Business Tax Burden in NH

Using tax rates to measure burdens over time is not a true measure of the impact that business taxes have on companies. Comparing state business tax climates using rates is problematic because of the various provisions of each state’s tax code that affect nominal rates. Here I assess business tax “burdens” using an economic measure – business tax collections as a percentage of private sector gross state product (GSP). This metric documents the state’s business tax burden placed on the total value of private sector goods and services produced in a state. Even using this measure of “burden” is problematic because it does not include all of the taxes, fees, and charges that may apply to a business in each state. Nevertheless, when it comes to addressing the primary sources of tax burden and the ‘headline taxes” that are identified with a state’s business climate, it is a better measure than looking at just business tax rates.

As the chart below shows, as a percentage of GSP, business tax burdens have nearly doubled in New Hampshire since the early 1990’s. Much of that is the result of the addition of the Business Enterprise Tax in 1993, as well as increases in the BET’s rate from 0.25% to 0.50% in 1999, to 0.75% in 2001. But some is also the result of increases in the rate of the business profits tax (BPT) which began the time period shown at 8.0% (from FY 92 through FY 93), dropped to 7.5% in FY 94 and hit a low of 7.0% (from FY 95 through FY 99) and finally rose to its current rate of 8.5% in FY 02. Importantly, the chart also shows that business tax revenue as a percentage of private sector gross state product has fallen since the recession and is now at a level seen at the beginning of the last decade. Again, changes in rules and a decline in wages and salaries both play a role in that decline. For comparison purposes the chart also shows the percentage of GSP that corporate income taxes take in Massachusetts, however, as noted, a number of other taxes are applied to or affect business in addition to corporate income taxes.

What’s Ailing the NH Economy?

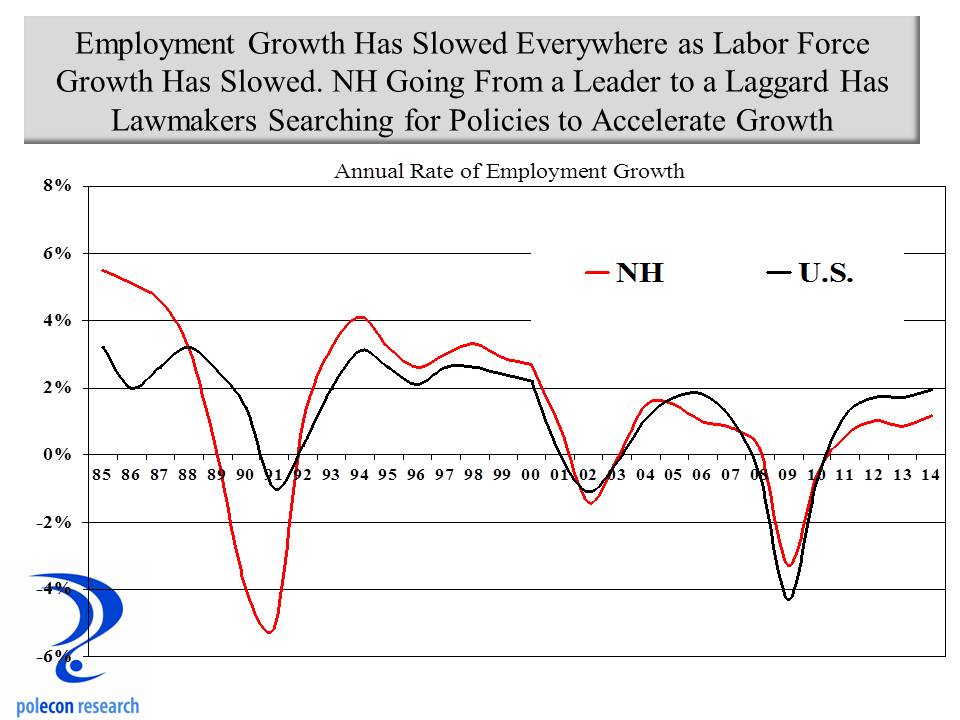

I don’t believe there has been a substantial, fundamental erosion of the ‘business climate” in NH. Slow labor force growth is by far the largest factor contributing to New Hampshire having gone from a leader to a laggard in job growth. That labor force issue is much broader and more complicated than the simplistic and too often noted “young people moving out-of-state.” The chart below shows that labor force growth has slowed more in NH than nationally in recent decades. Where once NH enjoyed a significant advantage in labor force growth, the state now lags the nation as a whole. Above average labor force growth is what allowed NH to have exceptional job growth in the 1980’s and much of the 1990’s.

Labor force growth (largely via in-migration of skilled, educated individuals and families from other states) provided NH with a resource advantage for decades. Slow labor force growth is now capping the amount job growth that is possible in the state. Some believe the state’s labor force would experience stronger growth if more job opportunities existed in NH and that simply reducing business taxes will make that happen. While that is true to a degree, today, businesses rarely locate where there is not clearly a sufficient supply of needed labor. A sharp rise in help-wanted advertising in NH in recent years even as private sector employment growth has remained relatively constant and disappointing (chart below) shows that in the near-term at least, demand for labor does not necessarily increase its supply. Significantly, the chart also shows that after a rapid rise in help wanted advertisements that was not accompanied by a noticeable increase in the rate of private sector job growth, help wanted ads have begun to decline in what may be a sign that employers, because of labor supply constraints, are increasingly looking elsewhere for labor.

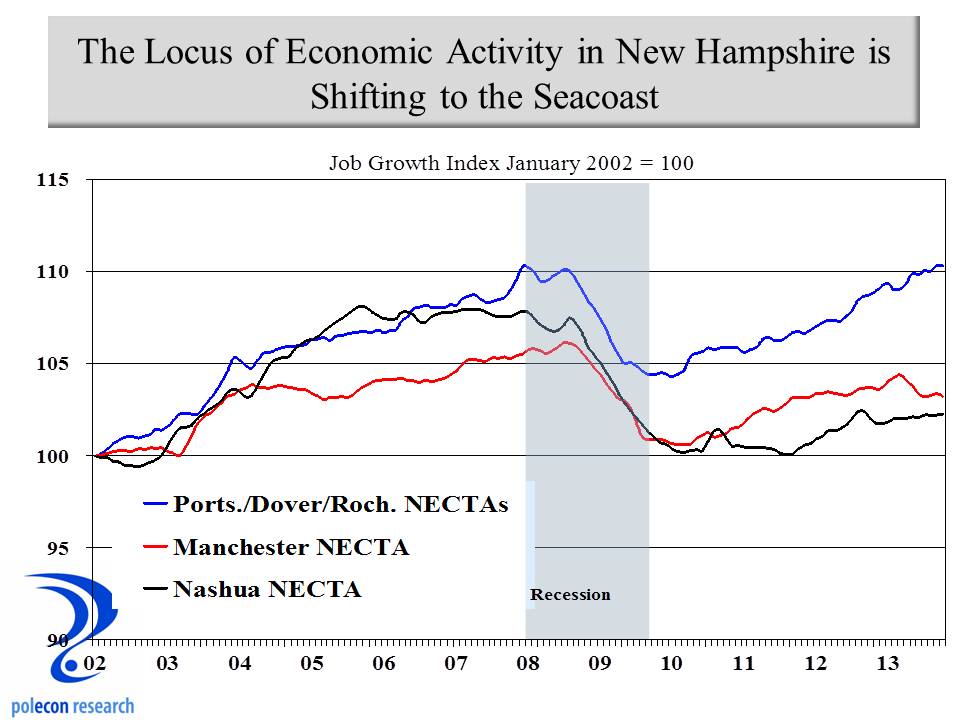

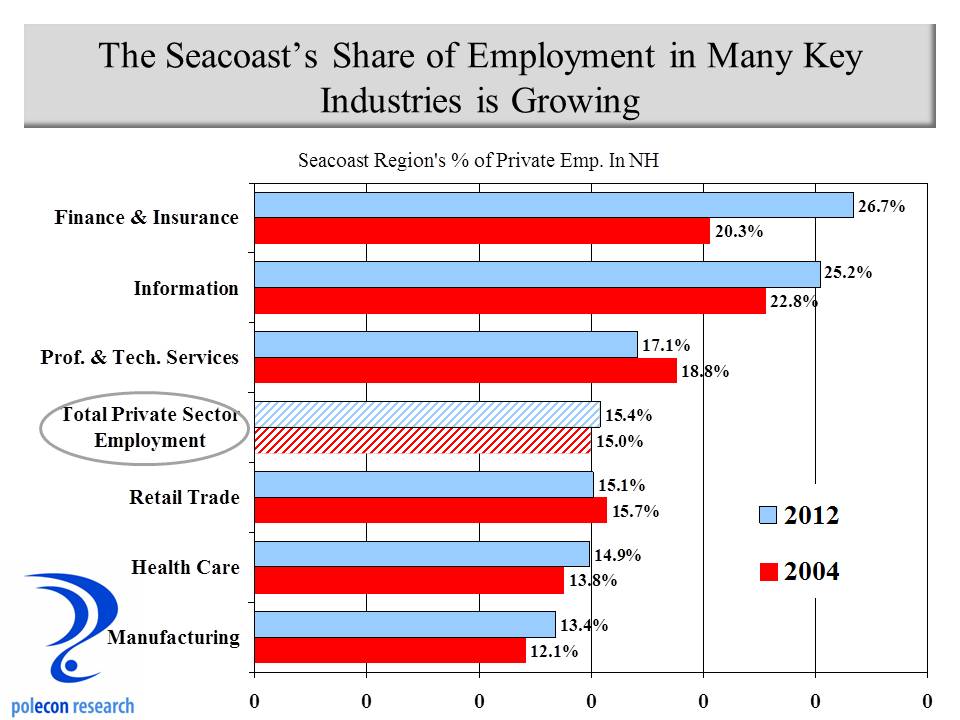

The demand for labor does generally increase the supply of labor but when the supply is growing slowly everywhere (especially in the Northeast where NH has typically attracted much of its increase in labor force), supply will respond accordingly. Increasingly businesses follow labor rather than the other way around and they do not rely on their demand to increase labor supply. Looking ahead, population and demographic projections show that both nationally and in NH, the working age population (defined here as age 18-64) will show almost no growth over the next 25 years. Competition for labor among businesses will become more intense and to keep and attract a labor force businesses will have to offer more than just the promise of a paycheck. I would argue that states and communities will also have to offer more (in terms of amenities – natural, social, civic, cultural, and services) to attract and retain the labor force needed for employment and economic growth. Evidence of the importance of amenities to labor supply (and employment growth) can be seen in the differential employment growth between some of NH’s regions such as the Seacoast (which has had higher population, labor force, and employment growth and which has several high amenity communities) and other regions of the state.

New Hampshire can improve its business taxes and business climate but whatever reforms are enacted, alone, are not going to overcome demographic and labor force imposed constraints on employment growth in the state. Lawmakers should, however, seek to assure that business taxes do not worsen key constraints on the NH economy moving forward.

The Longer-Term Problem

NH’s combination of a traditional tax on the profits of business profits (the business profits tax or BPT), along with its “business enterprise tax” or BET (on the combined compensation, interest, and dividends paid by businesses) may well exacerbate some of the disadvantages the state’s economy will face as a result of national and state demographic trends, making it more difficult for NH to overcome key constraints on employment growth in the state.

Reducing business tax rates that many see as too high is a near-term solution to a longer-term problem. The longer-term problem is slow or no labor force growth nationally and in NH in the coming decades that will limit profit growth everywhere but which will also place additional burdens on NH businesses. The labor force problem and NH’s reliance on business taxes will present NH businesses and state government with challenges that are unique to the state.

Wages and salaries are generally lower for comparable positions in NH than they are in Massachusetts. At one time it was easy to justify that wage differential because of large differences in the cost of living between the two states. Today, the cost of living differential between the two states has narrowed and NH is considered a high cost-of-living state. The U.S. Bureau of Economic Analysis (BEA) produces a “regional price parity index” Regional Price Parities (RPPs) measure the differences in the price levels of goods and services across states for a given year. RPPs are expressed as a percentage of the overall national price level (100). As the chart below shows (apologies for the poor quality – I lifted it directly from a BEA publication), NH (seen in red) has become a high cost state (largely because of housing costs), nearly as costly as Massachusetts.

In a state (NH) with living costs that are increasingly comparable to Massachusetts, workers in NH can be expected to seek wages nearly comparable to wages available in Massachusetts. For the most part, however, NH employees do not receive wages comparable to wages in Massachusetts and that contributes to some of NH businesses inability to hire needed workers and to NH’s modest job growth, despite increased job openings in the Granite State. It may also be a contributing factor to NH’s significant drop in its unemployment rate with only modest job growth (the unemployment rate is a residency-based measure that considers only whether or not a resident of NH has a job or not, regardless of where that job is located). Little or no growth in the labor force in the coming decades will increase competition for workers and will put more pressure on NH businesses to narrow wage and salary differentials with other, higher-cost states, if higher-skill jobs located in NH are going to grow. The catch 22 is that higher wages increase the BET liability of businesses at the same time they can reduce profitability (if productivity isn’t rising along with wages). A growing disconnect between the profitability of businesses in NH and the tax burden placed on them is not likely to be an incentive for businesses to compete for labor in a era when it is ever more scarce.

In a state (NH) with living costs that are increasingly comparable to Massachusetts, workers in NH can be expected to seek wages nearly comparable to wages available in Massachusetts. For the most part, however, NH employees do not receive wages comparable to wages in Massachusetts and that contributes to some of NH businesses inability to hire needed workers and to NH’s modest job growth, despite increased job openings in the Granite State. It may also be a contributing factor to NH’s significant drop in its unemployment rate with only modest job growth (the unemployment rate is a residency-based measure that considers only whether or not a resident of NH has a job or not, regardless of where that job is located). Little or no growth in the labor force in the coming decades will increase competition for workers and will put more pressure on NH businesses to narrow wage and salary differentials with other, higher-cost states, if higher-skill jobs located in NH are going to grow. The catch 22 is that higher wages increase the BET liability of businesses at the same time they can reduce profitability (if productivity isn’t rising along with wages). A growing disconnect between the profitability of businesses in NH and the tax burden placed on them is not likely to be an incentive for businesses to compete for labor in a era when it is ever more scarce.

Higher wages would not be a problem as long as productivity increases justify wage growth. When workers produce more they should see higher wages. Productivity growth has been modest over the past decade and shows little sign of accelerating. Thus increasing wages will likely mean slower profit growth for businesses in NH and elsewhere. I think we have seen the high mark nationally for corporate profitability for some time. But in NH, the higher wages needed to attract labor will also increase the business enterprise tax (BET) liability of companies. If profitability is indeed more modest because of faster wage growth and modest productivity growth, the BET liability of NH businesses relative to their business profits tax (BPT) liability will increase. An ad valorem tax on a resource (labor) in short supply with a rising price and that is paid regardless of the profitability of a business may increase (or cushion from decline) state revenue for a time but it also seems like a disincentive for businesses to pay the wages necessary to compete for labor and to hire in New Hampshire over the longer term.

New Hampshire’s tax structure has never really been a boon or an advantage for business but it has been attractive to large numbers of individuals and families over the years and it contributed to growth in the state’s labor force via inter-state migration into NH. Growth in key demographic groups within the labor force – skilled individuals with higher levels of educational attainment and regardless of their age ( two wage-earner, college educated, married couple families with children characterized the typical inter-state migrant to NH) made New Hampshire a much more attractive place for businesses to operate. The in-migration of “talent” fueled the state’s transition to a more sophisticated, technology dependent economy. But there is less state-to-state migration everywhere today and national and regional population, demographic, and labor force growth make it much less likely that NH will continue to realize those benefits from its fiscal structure. In the coming decades as competition for labor increases because of limited growth in the labor force, stronger wage growth will be needed to attract a limited pool of labor. Taxing compensation (as NH’s BET does) will increase tax liabilities for many NH businesses even as higher wages limit their profitability.

It is time for a discussion of NH’s business taxes, but that discussion needs to involve a lot more than just tax rates, credits, and how the rules apply to publicly traded companies.