The Outlook for Natural Gas Prices in New England

There is a lot of discussion, debate, advocacy and lobbying about whether New England’s energy future is becoming more vulnerable because of the region’s increasing reliance on natural gas for electricity generation. Some see the prospect of rising natural gas prices (because of increasing demand in the region and nationally) as a vulnerability and others are concerned about constraints on the pipelines that bring natural gas into the region. I’ve posted a lot about natural gas and electricity related issues and as I have previously stated my belief that regional increases in demand along with greater U.S. production of natural gas are more likely than not to create scenarios that will increase the capacity of the regional pipeline infrastructure. New England has traditionally been a region with a relatively low percentage of its energy consumption in the form of natural gas. That is changing rapidly, but increases in U.S. production of natural gas along with demand driven incentives to increase infrastructure capacity in the region should reduce a lot of the volatility of natural gas prices in New England.

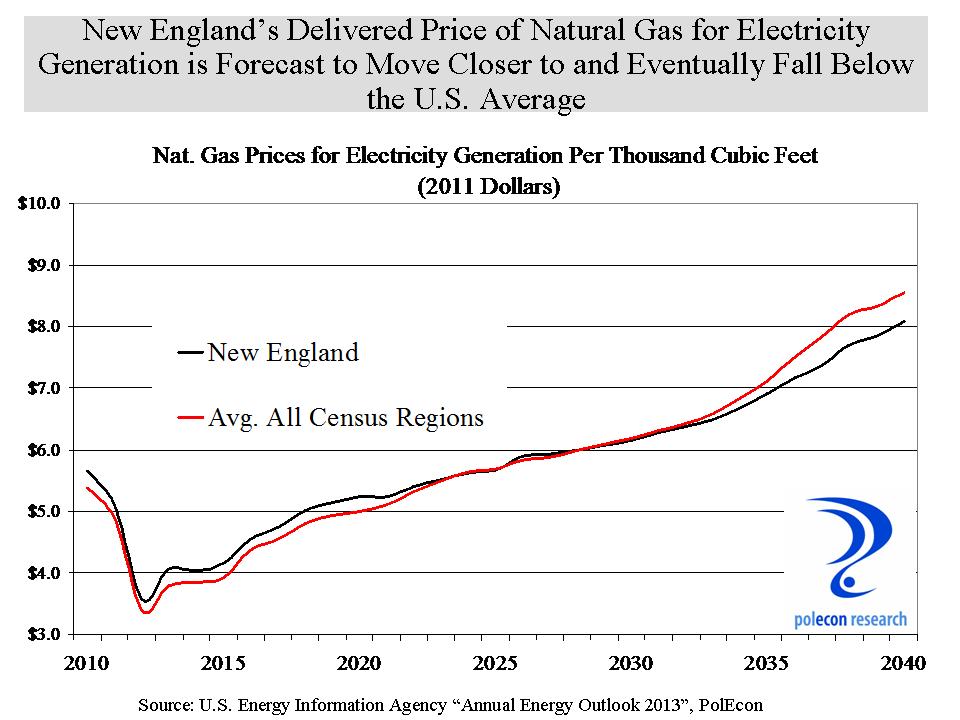

Apparently there are other folks who feel similarly. The U.S. Energy Information Agency (EIA) released its “Annual Energy Outlook” last month and it has a wealth of historical data, forecasts and projections. Their forecast of natural gas prices across the country are based on many economic, energy demand, production and other variables. They also produce a range of forecasts based on different assumptions about economic growth , energy demand and prices. The good news is that their baseline forecast for natural gas prices in New England (chart below) shows that prices in the region, which are traditionally higher than in most other regions of the country, are expected to align with the national average early in the next decade, and then move lower than the national average over time. Even better news is that this forecast is not dependent on a much weaker economy in New England than in the rest of the country (which would imply lower increases in energy demand in the region compared to the rest of the country). I don’t think EIA would be forecasting lower relative prices in New England if they did not see region’s pipeline infrastructure issue as being addressed.

The EIA also projects that the price of natural gas relative to coal will continue to increase. Coal will probably almost always be a cheaper fuel than natural gas but today’s typical “combined-cycle” natural gas generating facilities are much more efficient than coal-fired plants. When the ratio of natural gas prices to coal prices is approximately 1.5 or lower, a typical natural gas-fired combined-cycle plant has lower generating costs than a typical coal-fired plant. Natural gas-fired electricity generators enjoyed a strong competitive advantage over coal plants in 2012 but natural gas plants will begin to lose competitive advantage over time, as natural gas prices increase relative to coal prices. The retirement of older coal-fired generating plants, however, will mean that coal continues to generate a smaller percentage of the region’s and the nation’s electricity.

Some see New England’s increased use of natural gas as a concern. There are issues that need to be addressed but none that are insurmountable or that should have the region reconsider its increasing reliance on natural gas. Long-range energy price forecasts are notoriously difficult but New England’s energy needs and interests are finally becoming more aligned with the rest of the nation. For too long New England has been an anomaly as the most oil-dependent and least natural gas-dependent region in the country. Personally, I would rather have 300 million people concerned about my energy needs than just 15 million.

Explore posts in the same categories: Electricity, Electricity Generation, Energy, Natural GasTags: Electricity, forecast, Natural Gas, New England, price

You can comment below, or link to this permanent URL from your own site.

October 2, 2022 at 4:22 pm

Very thouughtful blog